The battle for the skies: Is free trade losing ground to protectionism?

The large commercial aircraft manufacturing market is increasingly threatened by trade barriers that can disrupt significantly a business until now dominated by Airbus and Boeing

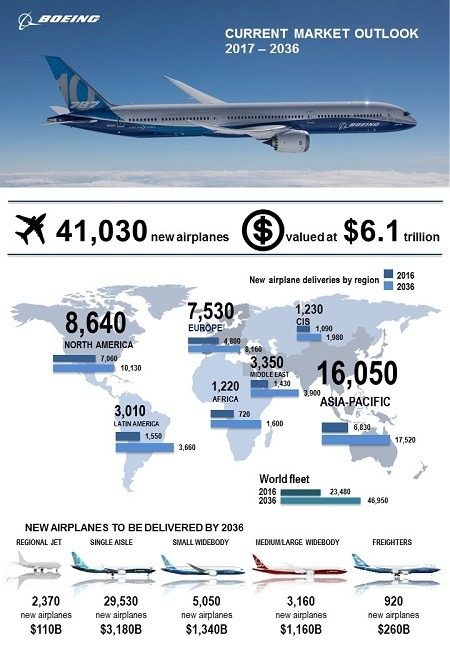

The large commercial aircraft market has become a symbol of globalization. Not only are customers spread worldwide –Boeing predicts that in 2036, ~60% of the global fleet will be based outside the US or EU[1]- but also supply chains: in Boeing’s latest model, the B-787, over 30% of its components come from overseas[2]. The high-tech component of commercial aircraft has enabled the duopoly of manufacturers –Airbus and Boeing- to be able to sell their products worldwide without excessive trade barriers. Aircrafts are difficult to substitute and highly complex to design and build. Therefore, even the most protectionist countries have been obliged to facilitate this trade.

That being said, from time to time there have been some protectionist claims by, not surprisingly, the home countries of the two duopolistic manufacturers: the US and EU. For example, the legal cross battle between them in the WTO[3] (regarding state subsidies) or what was called the Deal of the Century[4], a $35B contract for 179 tanker jets (based on commercial models) for the USAF that Boeing finally achieved after the USAF redesigned the bid which Airbus had won in the first place. Nevertheless, nothing very substantial or consequential.

Why then should the current protectionist wave across the world (including in the US and EU) be of any concern to aircraft manufacturers? Let’s consider which factors are changing in the industry, from Airbus perspective. First of all, the duopoly might eventually come to an end. Brazil, Canada, China, Russia and Japan[5] have national manufacturers which just recently entered or are planning to enter the market of large commercial aircraft (over 150 seats). Once powerful countries with large internal demand for jets (such as China or Russia) get their own national champions, will the incentives of free trade be wiped out? It might not be the case if the historical technical advantage prevails, but that is not certain. These new challengers rely during their first stages on western suppliers6 to make up for their technology gap and they profit from technology transfers that supply chain partners from Airbus and Boeing in those countries enjoy[7].

Secondly, even if the aforementioned were not to happen, a perverse example has been set in the industry: the successful bargaining of jet orders in exchange for industrial workload in the jet programs by the Chinese government. According to Airbus COO, and I quote, the rationale was the following: “There’s a direct connection between your investment, your capabilities to demonstrate that you care about the Chinese industry and at the same time your market access”[8]. How long until India demands the same bargain threatening manufacturers with higher tariffs?

Finally, Brexit, which for a pan-European manufacturer as Airbus could become a nightmare if the harshest version is implemented.

However, doubts remain. Could more offshoring mean more protectionism to preserve new national manufacturers? Could it create even more competitors? Is the most relevant risk of tariffs not in emerging economies but in the US and EU?

WORD COUNT: 800

- Boeing, Current Market Outlook, 2017: http://www.boeing.com/commercial/market/current-market-outlook-2017/

- Steve Denning, “What went wrong at Boeing”, Forbes, Jan 31 2013: https://www.forbes.com/sites/stevedenning/2013/01/21/what-went-wrong-at-boeing/#15ca29eb7b1b

- Shawn Donnan, Peggy Hollinger and Arthur Beesley, “US and EU both claim victory in Boeing-Airbus state aid dispute”, Financial Times, Jun 9 2017: https://www.ft.com/content/71cc85d4-4d2c-11e7-919a-1e14ce4af89b

- “EADS Abandons Airbus ‘Deal of the Century’”, Der Spiegel, Mar 9 2010: http://www.spiegel.de/international/europe/us-tanker-jet-eads-abandons-airbus-deal-of-the-century-a-682543.html

- Robert Wall, “New Jets Threaten Airbus and Boeing Duopoly”, Wall Street Journal, Jul 16 2017: https://www.wsj.com/articles/new-jets-threaten-airbus-and-boeing-duopoly-1500202802

- Christina Larson, “With 2 New Jets, Chinese Manufacturer May Become Global Contender”, New York Times, Nov 12 2014: https://www.nytimes.com/2014/11/13/business/international/with-2-new-jets-chinese-manufacturer-may-become-global-contender.html

- Howard Schneider, “GE ‘all in’ on aviation deal with China”, The Washington Post, Aug 22 2011: https://www.washingtonpost.com/business/economy/ge-all-in-on-aviation-deal-with-china/2011/07/17/gIQAgPmTXJ_story.html?utm_term=.a280e2fd7878

- “Airbus Chooses China for First Overseas Wide-Body Jet Plant”, Bloomberg News, Sep 19 2017: https://www.bloomberg.com/news/articles/2017-09-19/airbus-seeks-chinese-goodwill-with-first-overseas-wide-body-site

- Sarah Gordon, “Airbus – the European model”, Financial Times, May 23 2014: https://www.ft.com/content/c9a9a77c-db07-11e3-8273-00144feabdc0

- Julie Jonhsson, “A Trade War With China Would Be Bad News for Boeing”, Bloomberg, Nov 17 2016: https://www.bloomberg.com/news/articles/2016-11-17/a-trade-war-with-china-would-be-bad-news-for-boeing

- “Airbus Draws Line at Giving China its Own Widebody Jet Plant”, Bloomberg News, Mar 1 2016: https://www.bloomberg.com/news/articles/2016-03-02/airbus-draws-line-at-giving-china-its-own-wide-body-jet-plant

- Benjamin Zhang, “Airbus Draws Line at Giving China its Own Widebody Jet Plant”, Business Insider, Oct 16 2017: http://www.businessinsider.com/airbus-bombardier-c-series-boeing-tariffs-us-2017-10

- Christopher Jasper, “Airbus Warns New U.K. Government of Risk to Jobs, Fighter Role”, Bloomberg, Jun 8 2017: https://www.bloomberg.com/news/articles/2017-06-08/airbus-says-u-k-government-must-guarantee-mobility-to-save-jobs

- Cato Institute: https://www.cato.org/blog/airbus-beluga-how-bad-government-makes-cool-looking-things-sometimes

- Business Insider: http://www.businessinsider.com/airbus-bombardier-c-series-deal-challenges-2017-10

This is interesting, thanks for sharing. What will be interesting is the development of the non-duopolistic manufacturers. The new manufacturers in Brazil and China will need to have healthy sales from their own country to insulate themselves from protectionism in other countries. If they develop aircraft before their home market is mature and can solely fuel their demand, they expose themselves to risk of protectionism in other nations, like what happened to Bombardier. They’re almost incentivized to grow and develop not as quickly as possible, but in tandem with their home country.

Great article. Airbus seems to be caught in a real catch-22: spread out material sourcing and base manufacturing in return for foreign market access, while also feeling pressure to consolidate manufacturing processes to lower costs to compete. However, given Airbus’s fairly wide sourcing platform in Europe, the company should also try to leverage their scale with the EU to negotiate foreign trade and access agreements on their behalf.

I’m not well versed in aircraft sales/distribution, but I do believe that many smaller and regional airlines often purchase aircraft in second-hand markets, which further puts pressure on aircraft manufacturers to maintain existing sales relationships in the presence of increased competition. Airbus & Boeing could eventually be forced to focus increased sales attention to their military and non-civilian aircraft units, in which the products are much more complex and specialized.

Great article. I think that beyond protectionism and offshoring, the industry may inevitably lead the rise of competitors all over the world, mainly in emerging markets. Technology diffusion in the global world is happening every time faster, enabling new players to easily use Airbus’ and Boeing’s ‘intellectual property’; moreover, labor will continue being cheaper for the new players in emerging markets (with the strong drawback of lack of infrastructure). Additionally, and most important, as you mentioned, 60% of the demand will come outside the US and EU…

Reagarding the negative effects of the potential higher tarifs Airburs and Boeing might face to commercialize their aircrafts into Brazil, Canada, China, Russia and Japan, I would argue that these worldwide leaders will be obligated to implement a pass-through pricing strategy of the higher tariffs to customers into these specific economies (in case they implement such barriers for trade). Given the long production cycle of aircraft, and the technological and expertise gap between Boeing/Airbus and new competitors based in these countries, customers will still require to acquire from these leading aircraft manufacturers. The power of consumers or barriers of entry are minimal in this industry, where no perfect substitutes still exists in these economies.

Great article! I think the question of whether you should invest in production lines in a particular country depends on that country’s historical respect for outside investment. I would be wary from the perspective of Airbus or Boeing in building further capabilities and production lines in China. China’s history of flouting international IP law, nationalizing parts of businesses, and even reverse engineering other countries’ aircraft calls into question the wisdom of investing within that country. [1]

1. http://nationalinterest.org/feature/china-stole-fighter-russia%E2%80%94-its-coming-the-south-china-sea-17087

Great article, Sergio! I would like to add two points:

I believe there are arguments to believe that the scenario in which current producers of regional jets in emerging markets (like Embraer in Brazil) pose a threat to Boeing and Airbus’ monopoly is not very likely. Developing a new airplane model takes significant time and resources. For instance, the 787 program took Boeing more tan 10 years and a total investment of more tan U$32B (1). If one of the smaller players were to launch a larger airplane model, its development costs would probably be higher and the timeline would be longer, as the manufacturer would have to go through a steeper learning curve than Boeing. As we discussed in the FRC Boeing case, only in 2016, with more than 600 units delivered, the 787 project was reaching its projected unit cost. Given the complexity and scale required to make such a project sustainable, the risk for smaller manufacturers to try and break this duopoly that has been standing for decades is very significant.

As for your suggestion that Airbus should “double down its offshoring strategy”, I think that it entails a huge risk that should not be ommitted. Geographical diversification already makes Airbus’ supply chain very complex and risky. Manufacturing in countries in which the risk of trade policies being an obstacle to imports/exports is significant makes its supply chain significantly more vulnerable.

(1) “Boeing celebrates 787 delivery as program’s costs top 32 billion”, The Seattle Times, September 2011. https://www.seattletimes.com/business/boeing-celebrates-787-delivery-as-programs-costs-top-32-billion/

Extremely interesting look in a high-barrier industry, thank you. I was particularly intrigued by manufacturers’ use of offshoring to combat supply chain isolationism–this response is not intuitive, and mirrors a similar trend seen in a few other sectors like cloud computing. Given the possibility of protectionist tariffs in countries with nascent domestic aircraft producers, it seems like diversifying the supply chain is inherently risky–what if China imposes those tariffs tomorrow to protect its industry? On top of that such diversification leads to a risky and complex supply chain that is harder to manage and subject to more individual jurisdictions. However, I agree with you that there seems to be no better choice for the time being.

I think the critical next question is what kind of demand Airbus and Boeing are forecasting that those new airline manufacturers will see in the next 10-20 years. Presumably in some countries–like China–there will be incredible incentives to buy the domestically-produced, Chinese-owned airplane. Other countries may not erect such difficult barriers. Either way, a critical piece of this analysis is what impact the airlines expect those new players to have and their competitive responses. How much investment is there in new technologies like electric planes? Or moonshots/outside-the-box ideas like reintroducing supersonic flight? These are not revolutionary ideas, but clearly Airbus and Boeing must differentiate themselves somehow.

“Could more offshoring mean more protectionism to preserve new national manufacturers? Could it create even more competitors? Is the most relevant risk of tariffs not in emerging economies but in the US and EU?”

After reading this thoughtful piece, I was struck by two additional questions regarding the airline manufacturing sector amidst protectionist threats. How are firms considering the increased risks associated with decentralized operations; as we saw in one TOM case, overseas manufacturing increases exposure to diverse, unique economic climates. How do Boeing and Airbus consider fluctuations in currency value, labor and transportation costs, and governmental regulation, and mitigate these risks? In addition, heavy investment in local manufacturing is capital-intensive, making sales forecasting all the more important. How do the likes of Boeing and Airbus account for changes to their global supply chain when forecasting and preparing for future demand? What makes the protectionist threat even more interesting is that market leaders are not the only firms looking to decentralize their operations. For instance, Russian “military-industrial giant” Rostec is considering a cross-border partnership with the UAE to produce a commercial airplane (http://money.cnn.com/2017/11/13/news/companies/russia-rostec-uae-mc21-production/index.html). While I agree that market leaders must be cognizant of protectionist threats and take appropriate preventive measures, I also believe the risks inherent in having global operations are multifold. The airline manufacturing industry has relatively high barriers to entry, given the capital needed to undertake R&D and complete just one production run for example. As such, Airbus and Boeing may not need to act as swiftly as firms in other industries such as consumer technology, where being late to market perhaps poses greater risk of losing market share to established competitors or new entrants.