The HBS Digital Initiative reshapes digital to create a world where technology advances and serves humanity. The DI manages this forum to highlight perspectives from the HBS student community.

Want to learn more about technology and organizations? digital.hbs.edu

Technology changes habits. It seems like it was only a few years ago, when we had no choice but to go to the grocery store and wander around the shelves and be stuck in endless lines…

e-Grocery

E-grocery (or online grocery) depicts the business of the grocery domestic delivery to be arranged on digital platforms accessible by mobile apps [1]. This specific market has been rising in recent years, and the trend is still positive, as the 2018 Business Insider report indicates [2, 3]:

“Online grocery’s market value has grown from $12 billion in 2016 to $26 billion in 2018, suggesting that consumers are starting to get more comfortable ordering essentials and certain foods online. This newfound comfort, combined with the overall convenience of online grocery, is likely why the market is set to reach $117 billion in 2023.”

Figure 1 – Online Grocery Market Forecast

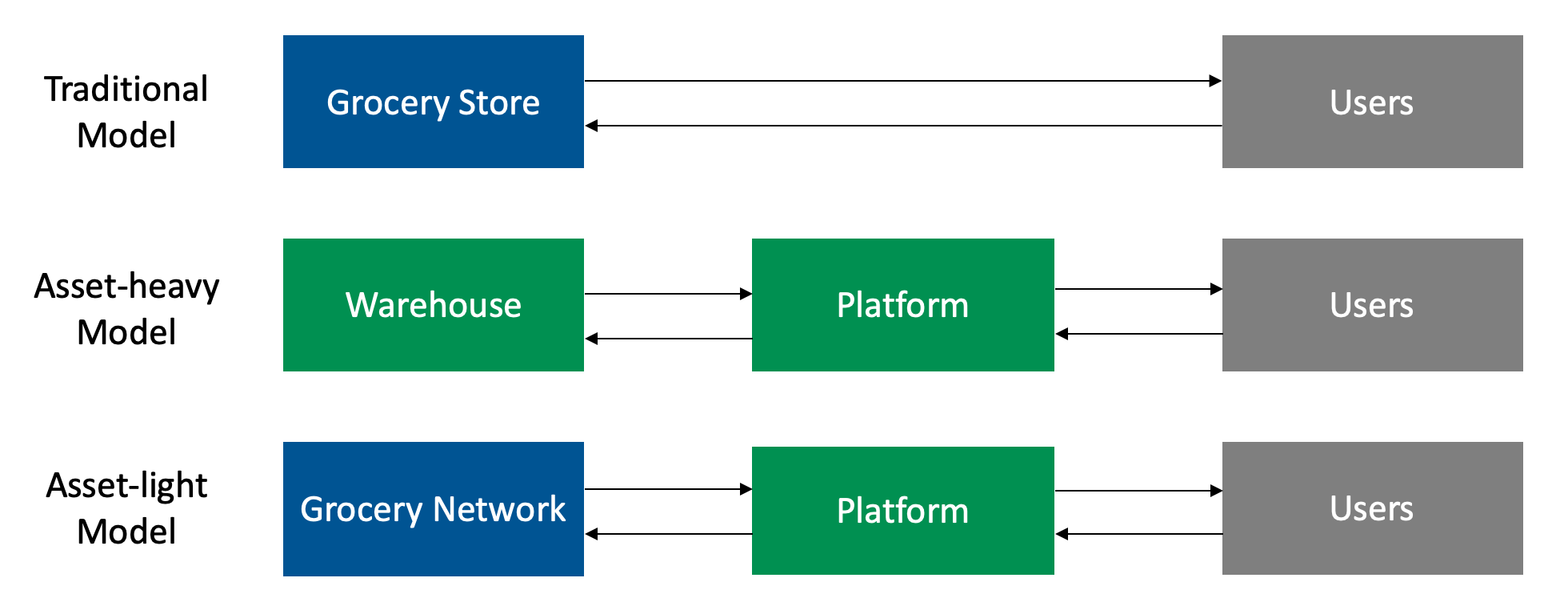

Following this trend, the main actors in this field (e.g. Amazon, Walmart, Costco, Peapod) have already invested tons of dollars to challenge traditional grocery delivery firms (Traditional Model, Figure 2) by establishing e-grocery business models. All these firms, however, adopted an asset-heavy model, as their operating models consist of both digital platforms, warehouse systems, and delivery fleets, and they are therefore supposed to replace entirely the downstream of the grocery retail supply chain (Asset-heavy Model, Figure 2).

In such a panorama, the question is: how might a start-up carve a space out, which could be sustainable over time?

This might be the story of Instacart, the $7.6bn company which succeeded by proposing to deliver your groceries right to your doorstep in an hour, as much as its competitors, but with a different operating model [4].

It was back in 2010, Seattle. Apoorva Mehta, a 25-year-old electrical engineer from the University of Waterloo, was working on the Fulfillment Engine project at Amazon, struggling to work out how to deliver packages more efficiently, when he decided to resign [6]. He thought Amazon’s model was unwieldy, since it requires warehouses to store perishable food, a fleet of painted trucks for logistics and workers to package and deliver the orders, which are costly and take time to set up [6].

In the pursuit of flexibility, he crafted a lighter model (Asset-light Model, Figure 2), in which a digital platform disintermediates the traditional store-customer physical relationship. But Instacart does not maintain warehouses or trucks, and the service leverages an existent network, as it is assembled out of already structured peers — existing supermarkets, shoppers and their vehicles [4, 5, 6].

When a customer places his order, he pays online to Instacart. The order goes directly to a shopper who then goes and visits stores to collect the required groceries. Shoppers pay the store through Instacart’s prepaid debit cards, and then they go to deliver to the customer. All the interactions are governed by a central digital platform, and this is how Instacart is able to place the groceries you have ordered to your doorstep in under an hour [7, 8].

Instacart’s success relies on the design of a matching platform where customers can surf and shop from many different stores directly from their devices, from large chains to specialty shops, and where a wide range of supply options are available.

This value is then captured in three ways [4, 6, 8]:

Delivery Fees: for every order processed, Instacart adds a standard delivery fee ($3.99-$9.99) depending on the purchased value and the requested delivery time.

Membership Fee: ‘Instacart Express’ is an annual membership fee priced at $99/year, which allows users to get free delivery of groceries.

Mark up Fee: Instacart set a mark-up of 15% or more from in-store prices on a few stores. However, in 2014, Meta realized that customers didn’t like the marked-up prices, and Instacart negotiated with suppliers to formalize a new pricing relationship. As a result, to date, most items on Instacart are now selling for the same prices as in stores.

To answer the first part of the question of the previous section, an asset-light operating model is not a sufficient, but instead a necessary condition to differentiate Instacart form its competitors. However, if we dive into the mechanics of the model, two conflictual elements materialize. Leveraging on existent supermarkets and flexible contract workers allowed Instacart to scale and to gain the benefits of network effects in a very short time. As a result, the platform’s positioning was quickly reinforced, preserving the resilience to market fluctuations at once. Scale created a ripple effect indeed, allowing Instacart to gain credibility to sign deals with new stores because of the user volume, and to gain new customers for the very same reason. But at what cost? Will Instacart be sustainable over time, if contract workers are reported to exist in a state of uneven working conditions, with few legal protections [9], and supermarkets are on the warpath because they are losing touch with customers and negotiating capacity with Instacart [10]? I hope you won’t bear a grudge with me if I have answered the second part of the question with another question.

References

[1] Punakivi, Mikko, and Juha Saranen. “Identifying the success factors in e-grocery home delivery.” International Journal of Retail & Distribution Management 29.4 (2001): 156-163.

[2] “The Digitally Engaged Food Shopper: Developing Your Omnichannel Collaboration Model: FMI”. 2019. Fmi.Org. https://www.fmi.org/forms/store/ProductFormPublic/the-digitally-engaged-food-shopper-developing-your-omnichannel-collaboration-model.

[3] “The Online Grocery Report: The Market, Drivers, Key Players, And Opportunities In A Rising Segment Of E-Commerce”. 2019. Business Insider. https://www.businessinsider.com/the-online-grocery-report-2019-1.

[6] “Apoorva Mehta At Startup School NY 2014”. 2019. Youtube. https://www.youtube.com/watch?v=wkmR7TYUt_c.

[7] “Grocery Deliveries In Sharing Economy”. 2019. Nytimes.Com. https://www.nytimes.com/2014/05/22/technology/personaltech/online-grocery-start-up-takes-page-from-sharing-services.html?module=inline.

[8] “Instacart’S Bet On Online Grocery Shopping”. 2019. Nytimes.Com. https://www.nytimes.com/2015/04/30/technology/personaltech/instacarts-bet-on-online-grocery-shopping.html.

[9] “Introducing Instacart’s New Earnings Structure For Shoppers”. 2019. Medium. https://medium.com/shopper-news/introducing-instacarts-new-earnings-structure-for-shoppers-26a11df53581.

I really liked the article. In the same category, Drizly is an alcohol E-commerce platform applying an asset-light model that operates in 70 cities in the US and is facing similar challenges. My only concern with these models is the question of trust: do customers trust the platforms to really reflect in-store prices? Do customers trust the person picking and delivering their items?

The online grocery market is growing at an incredible pace and I hope Instacart will not simply try to grow at any cost but will make sure not to erode its value proposition along the way.

Great post and analysis! I am a heavy user of Instacart as it makes my life so much easier. My alternative is drive or walk a couple of blocks away to some Cambridge supermarkets which is ok, but add two young kids to the equation and you’ve got yourself a huge mess. Instacart not only enables me not having to go with two tired and hungry children to the supermarket but also delivers the groceries to my door. Highlight on DOOR. Means I don’t need to take the bags out of the car into the elevator and one floor up the stairs.

Instacart has a Chilean equivalent, called Cornershop. It got acquired just last week by Uber!

This was certainty a great idea in 2010. However, while I do see value in the light asset set up of Instacart, I do think that it will be very hard, if not impossible, for them to compete with a behemoth like Amazon. Especially now, when Amazon is extending same day delivery, I can imagine that Amazon’s customers (especially prime members who don’t have to pay for delivery at all) will find it more convenient to do all their shopping on one platform, than to switch to a different platform to do their groceries and pay extra for delivery. Based on this, I do not believe that current business model of Instacart will allow them to be successful in the future.

Interesting post! I’ve never used Instacart, but I definitely understand the appeal of having groceries delivered to your door. I agree with your concern about the sustainability of this platform, however. Particularly now that there is some reputational risk for the retailers who partner with Instacart, I wonder if grocery stores will feel more pressure to figure out their own last mile delivery networks? Especially the big retailers like Costco and Publix. And if the big retailers leave the platform, will customers still see enough value in using Instacart?

I really liked the article. In the same category, Drizly is an alcohol E-commerce platform applying an asset-light model that operates in 70 cities in the US and is facing similar challenges. My only concern with these models is the question of trust: do customers trust the platforms to really reflect in-store prices? Do customers trust the person picking and delivering their items?

The online grocery market is growing at an incredible pace and I hope Instacart will not simply try to grow at any cost but will make sure not to erode its value proposition along the way.

Great post and analysis! I am a heavy user of Instacart as it makes my life so much easier. My alternative is drive or walk a couple of blocks away to some Cambridge supermarkets which is ok, but add two young kids to the equation and you’ve got yourself a huge mess. Instacart not only enables me not having to go with two tired and hungry children to the supermarket but also delivers the groceries to my door. Highlight on DOOR. Means I don’t need to take the bags out of the car into the elevator and one floor up the stairs.

Instacart has a Chilean equivalent, called Cornershop. It got acquired just last week by Uber!

This was certainty a great idea in 2010. However, while I do see value in the light asset set up of Instacart, I do think that it will be very hard, if not impossible, for them to compete with a behemoth like Amazon. Especially now, when Amazon is extending same day delivery, I can imagine that Amazon’s customers (especially prime members who don’t have to pay for delivery at all) will find it more convenient to do all their shopping on one platform, than to switch to a different platform to do their groceries and pay extra for delivery. Based on this, I do not believe that current business model of Instacart will allow them to be successful in the future.

Interesting post! I’ve never used Instacart, but I definitely understand the appeal of having groceries delivered to your door. I agree with your concern about the sustainability of this platform, however. Particularly now that there is some reputational risk for the retailers who partner with Instacart, I wonder if grocery stores will feel more pressure to figure out their own last mile delivery networks? Especially the big retailers like Costco and Publix. And if the big retailers leave the platform, will customers still see enough value in using Instacart?