Frontdoor – home services colossus with feet of clay?

Frontdoor boasts its huge and growing platform size (gained through great product), but is “tech-enabled platform” a PR label to woe the investors or a viable strategy remains the open question.

Frontdoor is the largest provider of home service warranties in the US. The value for its customers, homeowners, is a peace of mind due to removal of a hassle of going through uncertain and costly process of choosing handyman and paying out-of-pocket fees. Alike insurance company, Frontdoor charges homeowners an annual fee that provides coverage for home appliances or HVAC systems repair or replacement – the frequency of home service claims, however, is above 1.5x per year, much higher than other insurance protection (below 5% for auto or home insurances) [1].

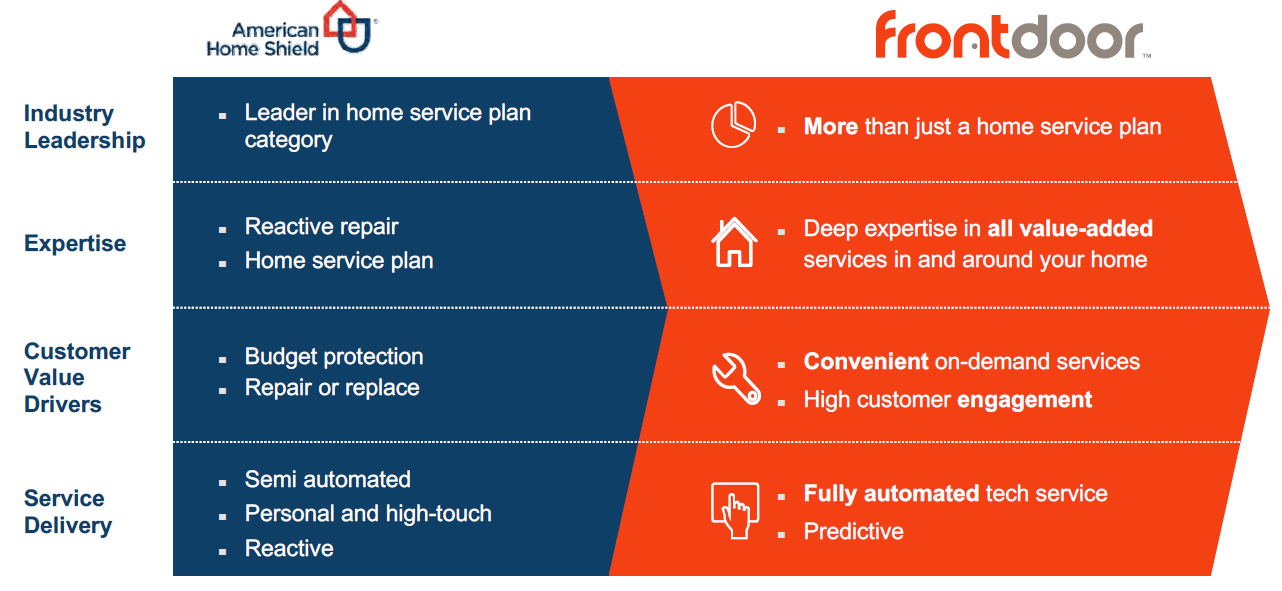

Based on almost 50 years history of this great product in the growing market for home services, in 2018 Frontdoor was spun off from its parent company, ServiceMaster, and re-positioned itself as a platform providing value to its huge base of contractors in addition to traditional customers, homeowners. The value for the contractors is claimed to be higher workload, cheaper and more certain leads to jobs, and other tech-services provided by the platform app.

Source: here and below – Frontdoor Investor Day 2018 presentation. https://investors.frontdoorhome.com/event/investor-day/investor-day

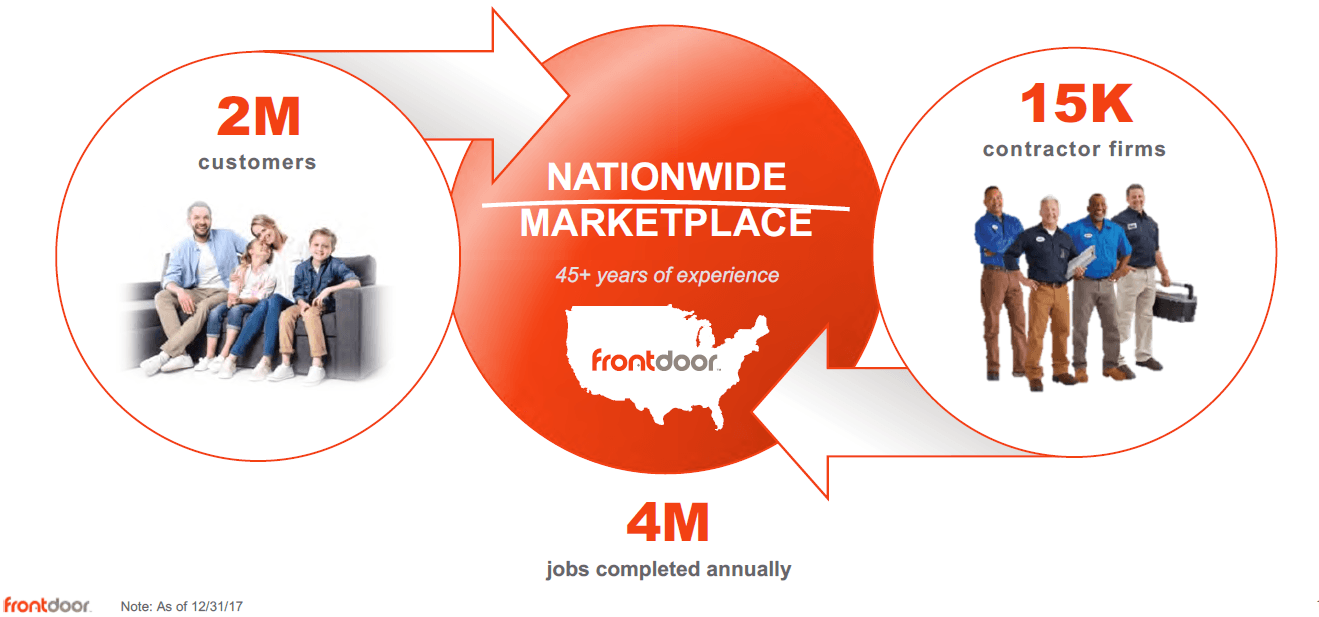

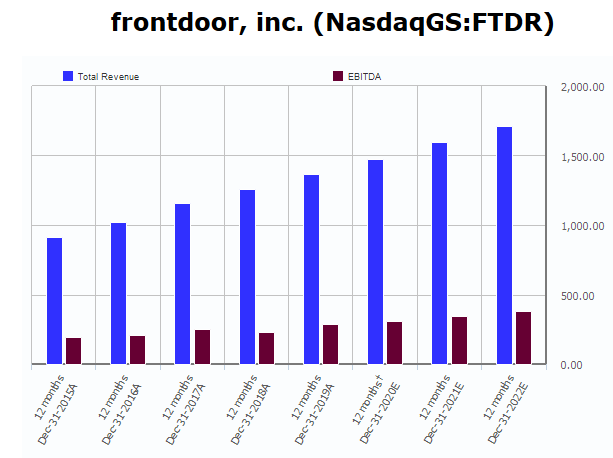

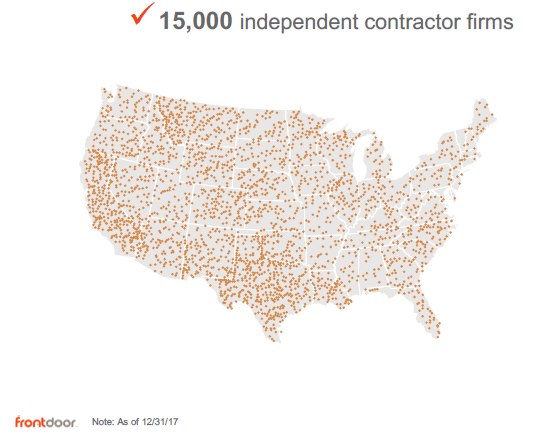

As of now Frontdoor services more than 2.1 mln customers through a team of approximately 2,000 employees and a nationwide network of more than 15,000 pre-qualified independent contractor firms that employ over 45,000 technicians.[1] The company has been growing its sales by around 10% annually over the past 5 years showing EBITDA and Net Income margins of around 20% and 10% respectively. This success has been appreciated by the investors (at least until COVID-19 outbreak) and sell-side forecasts continue to show growth for the company.

How sustainable is this platform model and are there fundamentals in place for the bright future of the company? The analysis below shows that Frontdoor faces challenges on all fronts in order to succeed.[2]

Source: S&P Capital IQ, accessed via Baker Library on 3/24/2020

- Strength of Network Effects: both homeowners and technicians have limited one-sided network effects as customers do not care about other people’s homes and technicians, if anything, lose from increased competition for the high-quality contractors. However, Frontdoor tries to create some positive effects for its large base of customers and contractors through the additional functionality of reviews on the platform. Frontdoor claims cross-side network effects via optimizing/leveling-out schedule based on large dispersed volume of workload on one side and huge number of technicians on the other. However, since one technician can actually serve around 1,000 customers per year (assuming 2-3 tasks per day) – adding a second technician brings only limited value for customers barring rare seasonal peaks of increased breakdown frequency.

- Network Clustering: Home service networks are naturally highly clustered by local areas since nor customers (tied to real estate) nor technicians (tied to their service centers) have high mobility. However, Frontdoor manages to squeeze value from its scale as it effectively provides lower replacement equipment prices by more effective bargaining with suppliers and better diversifying insurance risks.

Frontdoor has a huge network of contractors – but does it matter?

- Risk of Disintermediation: Similar to Homejoy, Frontdoor faces a risk of homeowners getting to know skillful technicians and then short-cutting Frontdoor. Despite insurance benefits that Frontdoor provides, the customers might be educated by the technicians about real frequency/repair costs of their specific appliance breakdowns and their ability to self-insure those limited costs.

- Vulnerability to Multi-Homing: On the supply side, given that home services provide relatively low and narrow scope of work for technicians, a contract exclusivity with Frontdoor seems to be a remote option. On the demand side, Frontdoor is better protected by a long one-year subscription which is most of the time renewed by the customers.

- Opportunities for Network Bridging: Apart from home services offering expansion Frontdoor has limited opportunities to engage more with the customers as the app is used rather infrequently (in fact, even now it’s mostly customers phone calls to the service center).

Overall, the key challenge for Frontdoor is how to add a more differentiated value to its platform. A few promising initiatives that the company pursues are: added tech services to technicians like communication app with the customers, remote appliance state diagnosis tools, parsing the huge accumulated data for better insurance risk pricing, etc. However, Frontdoor would need to move fast with those initiatives as traditional competitors, such as Angie’s List or Task Rabbit, are improving their own offers and could eventually add home services to their platforms. Moreover, similar players in home service plans industry are starting to move into the US market. One example is British HomeServe, which interestingly offers hardware products (both to increase value-add and reduce multi-homing) at its platform service: Tado, a smart thermostat, or LeakBot, a smart device which detects water leak.[3] Frontdoor so far has been pursuing a more aggressive and less strategic growth path adding non-insurance based on-demand service – Candu.

In his previous roles before Frontdoor its current CEO, Rex Tibbens, has been instrumental to growth of both Amazon and Lyft – what company Frontdoor will resemble more in the future?

____

[1] Frontdoor, Annual Report 2018. https://investors.frontdoorhome.com/sites/frontdoor3-e.investorhq.businesswire.com/files/doc_library/file/2018_Frontdoor_Annual_Report.pdf

Frontdoor Investor Day 2018 presentation.https://investors.frontdoorhome.com/event/investor-day/investor-day

[2] The analysis is based on framework suggested by Zhu, Feng, and Marco Iansiti. in “Why Some Platforms Thrive and Others Don’t.” Harvard Business Review 97, no. 1 (January–February 2019): 118–125.